The ambition of the Macron law of August 6, 2015, reforming employee share ownership, was to re-energize schemes for employee interest in share capital, such as the mechanism of warrants for business creator shares (BSPCE).

Indeed, BSPCEs are a loyalty tool, aimed at encouraging all employees to stay in the company and contribute to its development. This participatory management instrument is aimed at young companies with high growth potential, incorporated under the status of a joint-stock company.

The allocation of subscription warrants and the possibility of exercising them is therefore naturally conditioned by the presence of the employee in the company.

Consequently, the termination of the employment contract and the departure of the employee have direct consequences on the allocation of BSPCEs and on the definitive acquisition of the resulting shares.

That is why the parameters of this device must have been conscientiously designed and thought out to avoid disappointments, or even disputes. The hypothesis of the departure of a shareholder employee must thus have been anticipated during the elaboration of the conditions of allocation of subscription warrants.

What happens to BSPCE in the event of an employee's departure?

1- Interruption of the acquisition of allocated BSPCE

Generally, the allocation plans for share subscription warrants for company creators provide that these can only be exercised upon their definitive acquisition by the beneficiary.

This acquisition is made in instalments according to a predefined acquisition schedule. The longer the employee works within the company, the more BSPCE they acquire.

If the shareholder employee ceases to exercise his functions, the main condition for acquisition (= presence of the employee in the company) is no longer met and the acquisition is interrupted.

Consequently, all BSPCE issued but not acquired as of the departure date automatically become null and void.

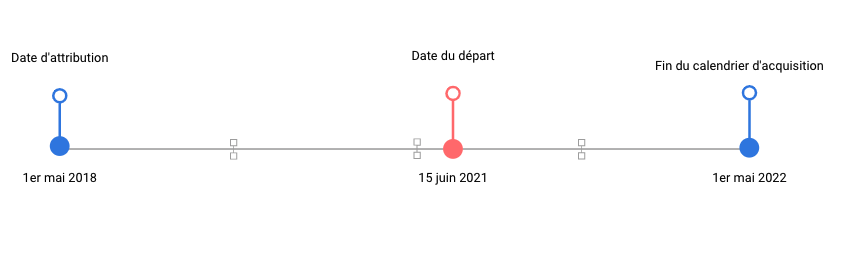

Example: Jean receives 400 BSPCE on May 1, 2018. His allocation plan provides for an acquisition schedule over 4 years with an acquisition of 25% at the end of each year of presence in the company.

On June 15, 2021, Jean leaves the issuing company. The acquisition of the allocated warrants is then automatically interrupted on this date:

➡️ At this date, he will have acquired 50% of his BSPCE (= 200);

➡️ The 200 non-acquired BSPCE are lost.

2- Reduction of the Exercise Period

When issuing the warrants, it is generally provided that their validity period is 10 years. However, most allocation plans provide for a reduction in the deadline in case of the employee's departure, or even its interruption.

Indeed, this allows the company to organize the end of the relationship it maintains with the employee and to protect itself against future unpredictability.

Thus, at the end of the period provided by the plan, the unexercised BSPCE automatically become null and void, and this before the end of the initially planned validity period.

As for the duration of the exercise period granted in case of departure, market practice converges on an exercise period of 3 months (6 months if the departure results from death or incapacity).

Nevertheless, it is up to the extraordinary general meeting or the delegation council to determine the period during which the warrants can be exercised, during the decision to allocate (article 163 bis G of the General Tax Code).

In a concern for fairness towards their employees, more and more companies are adapting the exercise periods. This is indeed the approach adopted at Equify. We have indeed chosen to propose a post-departure exercise period equivalent to the acquisition period validated by the employee. Thus, if an employee leaves the company 3 years after the allocation of his BSPCE, he benefits from a period of 3 years from his departure to exercise the distributed warrants and acquire shares.

It is also important to keep in mind that most allocation plans provide flexibility clauses, allowing the management team to offer the outgoing employee more advantageous deadlines.

Thus, in the event of termination of one of your employees' employment contracts, you can negotiate more flexible deadline terms if you feel that the conditions provided by the plan are too strict.

Start-ups can also integrate into their BSPCE distribution policy an acceleration clause. As its name indicates, it allows to accelerate the acquisition by the beneficiary of a part of his unacquired BSPCE at the time of departure.

Exercise of BSPCE by the outgoing employee

Following their departure, and subject to the respect of the imposed deadlines, the employee may choose to exercise the BSPCE acquired.

To assist you in managing such a possibility, here is a list of steps to take:

1️⃣ Receive a signed exercise notice from the beneficiary and verify that the corresponding exercise price has indeed been paid;

2️⃣ Have the capital increase resulting from the issuance of shares to the benefit of the beneficiary recorded by the governing body of your company (board of directors, management board or, where appropriate, the president) and update your bylaws;

3️⃣ Publish a notice in a legal announcements newspaper within the month following the signing of the decision recording the capital increase;

4️⃣ Finally, carry out the formalities related to your capital increase with the registry.

When it results from the implementation of an employee shareholding mechanism, the increase in share capital is governed by articles L225-17 to L225-150 of the Commercial Code.

Does your shareholder pact provide for a buy-back promise in case of departure?

To best manage the departure of an employee, your shareholder pact can organize their exit. It is indeed common to set out the financial terms of the departure of the employee shareholder, such as the conditions for the sale of the shares he holds.

Many pacts provide for a promise to buy back the shares of the outgoing employee for the benefit of all or part of the company's shareholders.

These sale or repurchase promises can notably provide for differentiated treatments between outgoing employee shareholders depending on whether they are "good leavers" or "bad leavers". This has an influence on the value of the shares, at the time of their resale.

The "good leaver" clause is intended to reward employees who have achieved the set objectives by allowing them to sell their shares at a favorable price. On the other hand, under the "bad leaver" clause, the shares allocated to the employee are sold at an unfavorable sale price corresponding to the original purchase price, without capital gain. It may concern the employee who has committed a serious or gross misconduct, but not only.

In 2016, the commercial chamber of the Cour de cassation validated the "bad leaver" clauses insofar as they apply in all types of dismissal, whatever the reason (Cass, com., 7 June 2016, 14-17.978).

If your shareholder pact provides for a promise to buy back the social shares, be sure to notify your shareholders of the employee's departure in order to allow them to exercise the option and buy back his shares.

As you will have understood, the departure of BSPCE beneficiaries can quickly become problematic in a company with significant employee shareholding.