Often overlooked, the tax regime of BSPCEs (share subscription warrants for company creators) is nevertheless one of the most favourable in Europe, both for the company that awards them and for its beneficiary. One more reason not to deprive oneself of them.

Share subscription warrants indeed benefit from very attractive taxation compared to other solutions for participating in share capital (free share allocation (AGA), stock options...).

Here is a quick summary of the key elements of this regime.

For the issuing company: no contribution

Unlike other employee share ownership schemes (options or free shares), the issuing company (or, where appropriate, the company employing the beneficiary in the event of intra-group allocation), is not liable for any contribution in respect of BSPCE allocations.

The issue of warrants has no tax impact. Indeed, whether it is at the time of allocation, at the time of exercise or even at the time of sale of the shares subscribed following the exercise of the warrants, no "employer" contribution is due.

By comparison, the issue of options or free shares can give rise to employer contributions of 20% to 30%.

For the title beneficiary: an attractive tax regime

The tax regime of BSPCEs is also very advantageous for the beneficiary in several aspects:

- The timing;

- The base;

- The tax rate.

When is the beneficiary taxed?

Taxation only occurs following the sale of the shares subscribed at the time of exercise of the BSPCEs. No tax is due before this sale, neither at the time of allocation, nor at the time of exercise.

This is one of the most important advantages of BSPCEs: the beneficiary only pays tax after having cashed in the capital gain made.

On what basis is the beneficiary taxed?

The rules for calculating the tax on BSPCE (Share Subscription Warrants for Employees) are very simple: the tax is based on the net capital gain from the sale, calculated by the difference between the sale price of the shares (net of any expenses and taxes potentially paid by the employee) and their subscription price at the time of the exercise of the subscription warrants (purchase price).

What is the applicable tax rate?

Article 163 bis G of the General Tax Code determines the terms of the taxation regime for capital gains from the sale of shares subscribed in the exercise of BSPCE.

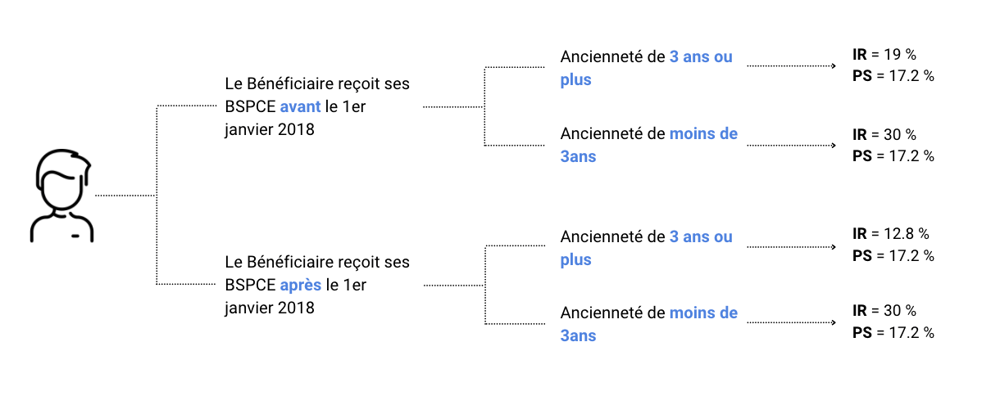

In reality, the tax regime applied to capital gains varies depending on the date of issuance of the BSPCE and the duration of the beneficiary's activity within the issuing company.

Indeed, following the finance law for 2018, the flat tax or single lump-sum withdrawal (PFU) applies to all net gains realized as part of the exercise of subscription warrants issued from January 1st, 2018.

There are 2 income tax rates applicable to the capital gain from the sale: a standard rate and an increased rate.

-

The standard rate

The goal of BSPCE being to retain employees, the standard tax rate only applies on the condition that on the day of the sale of the company's shares, the BSPCE beneficiary has been working in the company for at least three years. Otherwise, the capital gain is taxable at the increased rate.

Following the reform implemented in 2018, there are now 2 standard rates:

- For BSPCE awarded before January 1st, 2018: 19%;

- For BSPCE awarded from January 1st, 2018: 12.8%.

Finally, it is possible by exception to opt for taxation according to the progressive scale of income tax.

💡 Regardless of the chosen tax regime, a fixed deduction of €500,000 can be applied during the sale of SME shares by managers as part of their retirement.

Finally, whatever the case, acquisition gains or capital gains are also subject to social contributions at a global rate of 17.2% (rate applicable in January 2021).

In summary:

Illustration: Determination of the tax rate according to the holding period of BSPCE (rates applicable in January 2021)

Some Limitations

Unfortunately, it is not possible to combine the benefits of BSPCE with other mechanisms. Thus, BSPCE cannot be registered either on a stock savings plan (PEA) or on a company savings plan, notably on a company savings plan (PEE). The same applies to shares acquired in exercise of these BSPCE.

Reporting Obligations

The issuing company and the beneficiaries are subject to separate reporting obligations. These are taken up in Article 41 V bis of Annex III of the CGI.

For the company issuing the BSPCE: an individual statement and the DADS

Firstly, the company must establish an individual statement to be given to each beneficiary who has exercised his BSPCE. This statement must include the following information:

- Reason and registered office of the company;

- Identity and address of the beneficiary;

- Date of acquisition of the bonds;

- Number of shares acquired following the exercise of the bonds and acquisition price;

- Dates, number and acquisition price of the shares;

- Fraction of the French source gain;

- Seniority of the beneficiary in the company at the date of exercise of the bonds.

In the individual statement, the company will also certify that the bonds have been issued and allocated in accordance with the conditions provided for in Article 163 bis G of the CGI.

This individual statement must be given to the beneficiary no later than March 1 of the year following the exercise of the BSPCE.

Click HERE to download a free individual statement template.

Finally, the company must transmit this same information to the tax administration through the nominative social declaration (DADS) made for the year of subscription of the shares acquired in exercise of the BSPCE (Article 87 of the CGI).

For the beneficiary of the shares: income declaration for the year of sale

Beneficiaries must indicate on their income declaration the amount of the net capital gains from the sale, and this in the very year of the sale of the shares, under the conditions provided for in article 150-0 A of the CGI.

The beneficiary will have to keep during the entire recovery period (3 years in principle) the individual statement that will have been issued to him by the awarding company and give it to the tax administration on request only.

In case of omission of declaration or inaccuracies found in it or in case of failure to produce a liquidation statement to the tax administration, both issuing companies and BSPCE beneficiaries are liable to tax fines.