Employee shareholding

Focus on the register of securities movements

Digitize your corporate law: focus on maintaining the register of title movements!

In the face of a slowdown in Initial Public Offerings (IPOs) and a less dynamic mergers and acquisitions (M&A) market, how should the issue of liquidity for shareholders and employees of startups be approached today?

According to the founding principles of venture capital, investors and employee shareholders of startups reap the fruits of their investments and their work, either during the Initial Public Offering (IPO) or at the sale of their company. These two alternatives constitute for many the very purpose of any startup.

Unfortunately, the financial landscape has changed considerably in recent years with a slowdown in M&A operations and a significant decrease in the number of IPOs. This paradigm shift, which makes liquidity events more distant and less frequent, forces us to revisit the issue of liquidity for shareholders and employees of startups.

Over the past two years, we have seen a significant decrease in the number of initial public offerings and a major slowdown in mergers and acquisitions. This trend, due in part to economic and geopolitical factors, has had a major impact on the number and size of transactions, making liquidity opportunities less attractive and more rare.

Transaction volumes and values, 2019-2023 at the global level

This situation leads de facto to the first investors and first employees being forced to hold their shares beyond the duration they had potentially planned.

Faced with this new constraint, they may be tempted to favor short-term value creation scenarios, out of sync with a longer-term strategy adopted by the company's board. This divergence is of course likely to create tensions detrimental to good corporate governance.

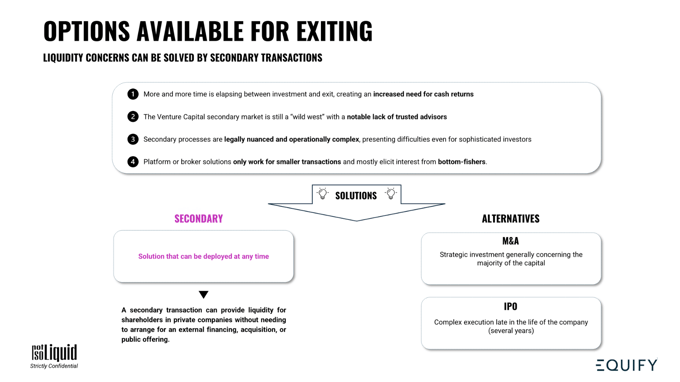

In a context where neither M&A nor IPO are seen as the preferred solutions for an exit today, the secondary is increasingly emerging as a complementary and necessary strategy that the company would do well to organize.

Before considering a secondary operation, it is essential to fully understand its own dynamics.

Unlike a traditional fundraising, the secondary is not aimed at providing new financing for the company, but at allowing a new investor to join the capitalization table in replacement of other shareholders (investors or employees) who will transfer their shares to him.

For the concerned shareholders, it is about offering them an opportunity to realize their gains, without having to wait for a possible initial public offering or an acquisition of the company.

Still poorly perceived in the ecosystem, a well-executed secondary operation with the right players can be a key step for the future of the company.

But for this, it is appropriate to deconstruct the myths that surround secondary operations, understand its rules, in order to make it notably a signal perceived as positive by the market.

If the objective is to withdraw from the capital the majority of the leaders and key employees of your company, there is no doubt that this approach will send a bad signal to the market. It is important to underline that this would also be the case for a primary financing round. This can suggest that the company no longer enjoys the trust and support of its main internal players, which can cause worry and skepticism among potential investors.

However, in some situations, the secondary can be a wise strategic choice. For example, if you are looking to replace shareholders who have already contributed all they could - whether in terms of resources, knowledge or skills - with new investors who are able to support you in the continuation of your project. In this case, the secondary can be a good signal for your Equity Story. It shows that the company is able to attract new investors, a sign of positive momentum and encouraging growth prospects.

Similarly, the secondary can be an excellent way to reward your employees. By offering them liquidity, you give them the opportunity to benefit directly from the success of the company. This approach can have a very positive impact on team morale and contribute to a motivating and rewarding corporate culture. Moreover, this new round, by showing that the company cares about the financial well-being of its employees, will be perceived positively both internally and externally. This can strengthen your reputation as an employer of choice and help you attract and retain talent.

Contrary to a commonly held idea, setting up a secondary financing round proves to be more complex than organizing a primary financing round. Several factors contribute to this complexity:

In short, all these combined factors make secondary financing more difficult to manage than primary financing. However, with good preparation and a dedicated team, it is quite possible to successfully navigate this complex process.

In a secondary operation, the shares that are put up for sale usually come from those who invested in the early financing rounds and are often classified as common shares. It is important to note that these shares are not the same as the preferred shares that were issued during the last fundraising. The latter generally have superior protections and therefore offer a better level of security to investors. Consequently, it would be logical to apply a discount, or a reduction in price, to the shares that are sold during a secondary round. Moreover, we live in a context where valuations tend to decrease between each round. This reinforces the idea that it is all the more important to consider a price adjustment when selling shares during a secondary operation.

It is important to note that all the actors involved in a secondary operation are not necessarily well informed about the details of the shares and their conversion process, especially the employees of your company. Indeed, the complexity of this information can sometimes make their understanding difficult. Therefore, it is wise to adopt a proactive strategy of education and communication. For example, organizing an annual information session on the sale conditions of BSPCE, their exercise price and other relevant information, can be extremely beneficial. The main objective of this approach is to make employee share ownership as transparent and understandable as possible for all employees. This would avoid misunderstandings from turning employee share ownership into a myth, which could prove disappointing for those who do not have the appropriate information.

Generally, a secondary operation is initiated either by the investment fund holding shares in the company, or by the company itself. In either case, several preliminary steps are essential. First, it is necessary to confirm the right timing of the operation, taking into account the economic context and the financial situation of the company. Then, it is important to define a precise schedule for the operation, in order to best organize the different stages and avoid any delay. In addition, it is necessary to identify the concerned shareholders in order to carry out their identity verification (KYC). This step allows to ensure the legitimacy of the shareholders and to prevent possible frauds. All these preparations are necessary to guarantee the smooth running of the secondary operation.

It is strongly recommended to avoid as much as possible preferential liquidation clauses, and especially any clause that stands out from the 1x participating standard. These clauses, when particularly aggressive, can often be a symptom of a company in a precarious situation or in difficulty. In such a situation, considering a secondary operation is certainly not the best strategy. Indeed, this could add an additional layer of complexity and risk to an already unstable context. Therefore, faced with aggressive preferential liquidation clauses, it is better to be cautious and avoid the secondary.

💡 As a reminder, preferential liquidation clauses protect the investor in case of unsatisfactory performance of the company. These clauses allow investors who benefit from them to obtain a larger share of the price than they would normally have received by a proportional distribution of capital.

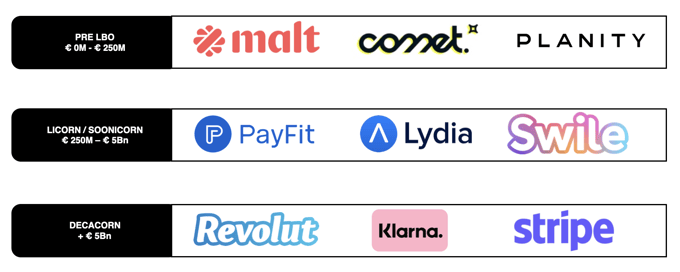

Examples of companies that have carried out a secondary operation by stage of development:

Source : Webinar, Pitchbook, Global M&A Industry Trends - Février 2024 (PwC)

Digitize your corporate law: focus on maintaining the register of title movements!

Involve your employees and corporate officers in the capital and results of your company through the stock options scheme!

The exercise schedule, known as "vesting", is an important modality of the BSPCE allocation plan. What are the best practices in this area?